On Saturday, the National Statistics Office (NSO) released its August economic update.

This article breaks down the key data points and policy factors that shaped Vietnam’s economic landscape in August 2025.

Key developments

The State Bank announced it would dip into its reserves again.

The State Bank of Vietnam (SBV) announced on August 23 that it would resume selling foreign currency through forward contracts to credit institutions with negative US dollar positions.

This is likely to put the local currency in even riskier territory than it is already — Vietnam’s ForEx reserves are currently sitting around US$80 billion, which is enough to cover two months’ worth of imports but not the three the IMF recommends.

Of note, the State Bank does not regularly report on its reserve holdings, and so exactly how this plays out probably won’t be known until some time after the fact.

Fitch warned credit-powered growth was risky.

In a statement on its website published August 16, Fitch Ratings warned that Vietnam’s push for rapid economic growth despite higher US tariffs could “aggravate leverage-related weaknesses”.

One of the biggest, most highly respected, and credible credit ratings agencies in the world, Fitch Ratings’ assessments often carry a lot of weight with foreign investors.

Bank quarterly reports showed bad debts continue to increase.

Bad debt across 28 Vietnamese banks rose to VND 294.2 trillion or US$11.32 billion by June 2025, up more than 12 percent since the start of the year, it was reported.

This fits with the risks mentioned earlier with respect to credit-powered growth.

Macroeconomy

Currency

The Vietnamese dong continued to devalue against the greenback.

The State Bank of Vietnam (SBV) opened the month with the central exchange rate at VND 25,058 to the dollar, but by August 29, it was trading at VND 25,240, an increase of VND 182 or 0.73 percent.

Conversely, the black market mid-market rates started the month at 26,445, jumping 240 dong to VND 26,685 by the end.

Interventions through open market operations also continued — the US dollar injection mentioned earlier, but also about US$13.73 billion in 7, 14, 21, and 90-day reverse repo transactions took place.

All of that is to say there is a lot of pressure on the SBV’s managed peg, with the bank favouring short-term fixes over long-term policy changes.

See also: How Low Can the Vietnamese Dong Go?

Inflation

Core inflation climbed, but headline inflation remained mostly steady.

Inflation climbed a little in August, reaching just 3.24 percent year-on-year, up from 3.19 percent in July.

Conversely, core inflation dipped to 3.25 percent, down from 3.3 percent.

This suggests price regulations are doing some heavy lifting, specifically in electricity and fuel.

It’s not clear how long this can last without doing some serious damage to the energy sector (state-power provider EVN is already holding VND 44 trillion in accumulated losses).

Manufacturing

Manufacturing recorded a continued expansion.

Vietnam’s Industrial Production Index (IIP) showed continued growth in August, rising 0.5 percent month-on-month.

Similarly, S&P’s Purchasing Manager’s Index showed Vietnam’s manufacturing sector continuing to grow, despite recording a fall in new export orders.

The index eased to 50.4 in August, down from 52.4 in July, signalling the sector is still marginally improving.

Trade

Trade continued to expand.

Imports shrank by about .8 percent, but exports climbed 2.6 percent.

This comes after the 20 percent US tariff was applied, which it was expected would see Vietnam’s exports dip.

However, Vietnam’s 20 percent is still 10 percent lower than the 30 percent applied to goods from China, and with no guidance on what constitutes transhipment, it would make sense if Chinese companies with the means were redirecting their goods through Vietnam.

Incidentally, China’s exports to the US in August were down 33 percent.

Moreover, newly registered FDI from Vietnam’s neighbour to the north was US$2.65 billion for the first eight months of the year.

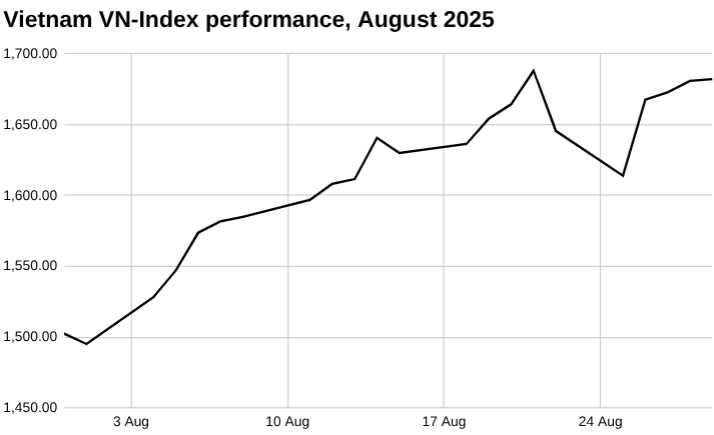

Stock Market

The stock market went gangbusters.

The VN-Index reached 1,688.42 on August 21, the highest it had ever been.

By the end of the month, it was up 11.96 percent over the start.

That said, foreign investors continued to net-exit the market to the tune of a little under US$1.6 billion.

Moreover, there has been no change significant enough to really explain why the market is as high as it is, and therefore, it looks like hype may be playing an outsized role in pushing stock values up.

See also: Vietnam Stock Market Outlook: September 2025

What to watch in September

This time of year in Vietnam manufacturing usually picks up in anticipation of the Christmas shopping season in the Western hemisphere.

However, on account of the Trump tariffs, a lot of firms brought forward orders to the start of the year, which has led to many observers suggesting a decline in exports in the back end of 2025.

That said, given exports have continued to rise in spite of the tariffs, and that Vietnam’s IIP and PMI have stayed in growth territory, that may not be the case.

It is, however, only early days in this new 20 percent tariff regime; moreover, with a US court ruling the tariffs illegal, everything could be upended once again in the near future.