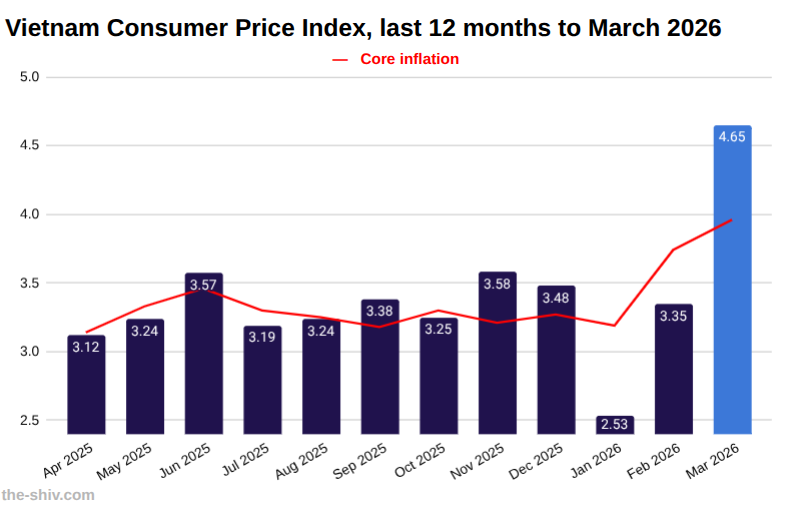

Vietnam’s Consumer Price Index (CPI) climbed from 3.35 percent year-on-year in February to 4.65 percent in March. Here’s how it happened and where it might be headed, with inputs from Michael Kokalari, Chief Economist at VinaCapital, and Vicente Nguyen, Chief Investment Officer at Asia Frontier Capital.

Vietnam’s National Statistics Office (NSO) reported an increase in the price of gasoline in March of 29.72 percent compared to February, with the price of diesel up 57.03 percent, on the back of rising energy prices from Iran’s de facto closure of the Strait of Hormuz.

This saw Vietnam’s Consumer Price Index (CPI) climb from 3.35 percent year-on-year in February to 4.65 percent in March.

Above the government’s target of an average of 4.5 percent for the year, this has been cause for some concern, though it could have been worse, Michael Kokalari, Chief Economist at VinaCapital, told the-shiv.

“Had they (the government) not… suppressed the price of petrol going higher it would have been like five and a half or so percent CPI,” he said.

That is, throughout March, the government of Vietnam dipped into a Price Stabilisation Fund set up to collect extra on each litre of fuel sold when prices are low to use to subsidise prices when they are high.

Kokalari, however, went on to say price management efforts thus far still may not be enough.

“They’ll also have to, at some point, do some measures directly to help households, maybe some sort of a mortgage or interest rate subsidy or something like that,” he said.

Conversely, Vicente Nguyen, Chief Investment Officer at Asia Frontier Capital, was a little more circumspect.

He told the-shiv that though fuel prices have risen, food prices are what really matter.

“The rice price and pork prices are the most important factors of the CPI, and at the moment… those goods are still very stable — the rice price hasn’t moved up, and the pork price has even declined,” he told the-shiv.

This was reflected in the NSO’s March data, which showed rice prices decreased by 0.06 percent, with the pork price falling by 2.9 percent.

Nguyen also said fuel prices, though volatile, may be levelling off.

“This is, I think, already the peak of diesel oil in the domestic market,” he said.

Nevertheless, he did raise concerns that the rising CPI could presented a significant threat to the government’s self-imposed GDP growth target of 10 percent for the year.

This target was reinforced last week, when the new Prime Minister of Vietnam, Le Minh Hung, referred to it as a “development imperative” in his inaugural address to Vietnam’s National Assembly.

This was already ambitious and in the current global fuel crisis context, seems even more so.

In his Monthly Macroeconomic Summary, Kokalari speculated that the war could shave up to 1 percent off Vietnam’s 2026 GDP growth.

Nguyen also said 7 to 8 percent growth was more likely, with 10 percent being “quite tough indeed.”

The government, however, looks intent on meeting its commitment.

Following a meeting with the new prime minister last week, it was announced that 42 banks had agreed to lower their interest rates, with the prime minister promising the support of the State Bank in managing liquidity — whereas bank-to-bank overnight interest rates have at times reached double digits in the last few months, reverse repo transactions have been held steady at 4.5 percent.

That said, lower interest rates are likely to strain the local currency’s floating peg.

In recent years, these sorts of devaluation pressures have largely been managed through open market operations and utilising Vietnam’s foreign currency reserves.

Vietnam, however, has only roughly US$80 billion in foreign currency reserves left, which is only about two months’ worth of import coverage against a recommended three. (Though note the SBV doesn’t regularly update the public on its foreign currency holdings).

The alternative, however, letting the dong devalue, doesn’t have a lot of political support.

Kokalari told the-shiv the government’s focus is on foreign direct investment, with a stable currency seen as a key selling point.

“If they did let the currency depreciate, I think what you would see is like very small steady increments, not all at once, to try to make it very smooth to make investors feel comfortable,” he said.

Instead, Kokalari said he expects interest rates to be allowed to move higher, though not policy rates, but commercial banks’ deposit interest rates instead.

Nguyen was of the same mind, pointing out the government has few other options.

He also went on to say that Vietnam’s experience with high inflation in the past, and the government’s success keeping it in check over the last decade will likely be a deterrent from high growth policies that put inflation second.

“They don’t want to ruin or destroy all the achievements they already had in the last 10 years. So I think they will not sacrifice inflation for economic growth,” he said.

Source materials

Vicente Nguyen: Video / Audio / Transcript

Michael Kokalari: Video / Audio / Transcript