Contents

ToggleDisclaimer: The author of this Outlook does not own any stocks or have any financial interest in the performance of any of Vietnam’s stock markets.

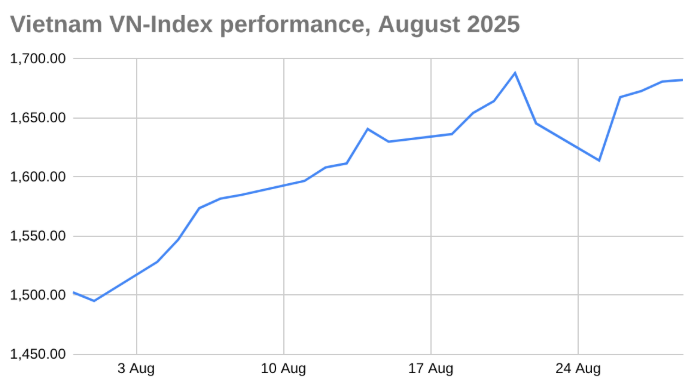

The year 2025 has been an interesting year for the Ho Chi Minh City Stock Exchange (HoSE), which has broken a number of records, climbing well above its previous high of 1,528.57 points recorded back in 2022.

Last month was no exception, with the VN-Index recording big gains and liquidity jumping significantly.

Here’s how Vietnam’s stock market performed in August and what that might mean moving forward into September.

It's free to keep reading but you will need to sign in.

VN Index August performance

The VN-Index closed Friday, August 29, 2025, at 1,682.21 points, a gain of 179.69 points since the start of the month, a gain of 11.96 percent.

This also put the key index up almost 33 percent since the start of the year.

Market capitalisation

The market capitalisation of the HoSE reached VND 7,275 trillion or US$271.6 billion by the end of August.

This was up from VND 5,220 trillion or US$198.1 billion in January.

VN30 August performance

A similar rise was seen in Vietnam’s VN30, which gained 250.15 points or 15.49 percent in August.

There were broad gains across the board, with just seven stocks recording declines in their stock price.

These were:

- Real estate developer Becamex IDC Corp. (BCM);

- PV Gas (GAS);

- Vietnam Rubber Group (GVR);

- Beer maker Sabeco (SAB),

- Technology firm FPT Corporation (FPT),

- Vietnam’s biggest dairy producer, Vinamilk (VNM), and

- National petrol chain, Petrolimex (PLX).

Collectively, these stocks pulled the index down by about 2.76 percent.

Conversely, the stocks that pushed the index up were:

- Conglomerate (though mostly real estate) Vingroup (VIC);

- LienViet Post Bank (LPB);

- Retailer (groceries and electronics), Mobile World Investment Corporation (MWG);

- VPBank (VPB); and

- Real estate developer and subsidiary of Vingroup, Vinhomes (VHM).

Collectively, these stocks accounted for 46.74 percent of the index’s gains.

Trading activity in Vietnam

August saw a significant spike in liquidity, with order-matching value rising to VND 982.6 trillion (US$37.3 billion) from VND 757.4 trillion (US$28.7 billion) in July.

The average daily trading value was VND 46.8 trillion or about US$1.8 billion.

This was well above the daily average for the first six months of the year, which was about VND 17 trillion (US$645.3 million).

This increased liquidity fits with expanded media coverage of the local bourse driving hype, combined with a push to increase cash in the economy through bank lending.

Foreign investor flows (HoSE)

Of note, investing abroad for Vietnamese is strictly regulated. Foreign investors, however, are able to more freely move their money in and out of the country. This is worth keeping in mind when comparing the behaviour of foreign versus local investors.

In August, foreign investors net-exited the HoSE to the tune of VND 42.2 trillion, about US$1.6 billion.

A large part of this was South Korea’s SK Group divesting from Vietnam’s Vingroup.

The exact value of the sale has not been reported, but it looks to be several hundred million dollars — foreign ownership of Vingroup shares fell by just over 44 percent over the course of the month.

Vingroup, however, was not alone, with 21 of the 30 stocks in the VN30 net-sold by foreigners.

All up, foreign holdings of shares in the VN30 were down by 1.89 percent by the end of the month.

This is part of an ongoing pattern with about US$6.2 billion of foreign holdings sold off since the start of 2024.

Vietnam Foreign Room Limits Securities (VN30) September 2025

| Ticker | July 31 | August 29 | Change | Remaining |

|---|---|---|---|---|

| Total | 20,840,960,070 | 20,446,402,593 | -394,557,477 | -1,383,209,006 |

| VIC | 264,902,144 | 148,231,372 | -116,670,772 | 1,714,171,090 |

| GVR | 29,239,832 | 22,040,207 | -7,199,625 | 497,959,793 |

| LPB | 27,760,621 | 25,510,823 | -2,249,798 | 123,853,282 |

| HPG | 1,686,694,351 | 1,568,945,760 | -117,748,591 | 2,192,032,508 |

| SSI | 826,840,991 | 785,210,102 | -41,630,889 | 1,188,653,816 |

| VRE | 429,506,452 | 410,967,944 | -18,538,508 | 730,153,076 |

| VHM | 430,495,053 | 415,444,821 | -15,050,232 | 1,638,261,181 |

| PLX | 218,233,511 | 211,159,955 | -7,073,556 | 47,615,661 |

| VPB | 2,041,611,345 | 1,988,701,650 | -52,909,695 | 391,475,430 |

| SHB | 216,163,545 | 211,602,956 | -4,560,589 | 1,008,121,144 |

| CTG | 1,461,443,413 | 1,432,083,207 | -29,360,206 | 178,914,317 |

| MWG | 724,136,357 | 712,151,393 | -11,984,964 | 12,898,263 |

| STB | 376,960,807 | 371,878,220 | -5,082,587 | 193,686,494 |

| GAS | 43,134,793 | 42,568,681 | -566,112 | 1,105,341,049 |

| VCB | 1,837,859,181 | 1,823,073,933 | -14,785,248 | 683,628,595 |

| VNM | 1,025,289,470 | 1,017,431,857 | -7,857,613 | 1,072,523,588 |

| MBB | 1,417,618,203 | 1,407,500,031 | -10,118,172 | 10,369,123 |

| MSN | 385,689,081 | 383,199,771 | -2,489,310 | 1,129,728,316 |

| SAB | 756,035,123 | 751,469,348 | -4,565,775 | 531,093,024 |

| BID | 1,226,627,956 | 1,221,395,014 | -5,232,942 | 885,013,561 |

| BVH | 202,278,011 | 201,590,816 | -687,195 | 162,147,338 |

| ACB | 1,540,937,979 | 1,540,938,686 | 707 | 58,293 |

| HDB | 611,200,479 | 613,490,865 | 2,290,386 | 784,029 |

| TCB | 1,590,552,461 | 1,596,659,971 | 6,107,510 | -6,107,510 |

| BCM | 22,047,203 | 22,175,403 | 128,200 | 329,724,597 |

| VJC | 42,584,177 | 43,178,223 | 594,046 | 119,305,177 |

| TPB | 646,600,555 | 659,477,575 | 12,877,020 | 133,109,283 |

| FPT | 601,137,060 | 639,148,890 | 38,011,830 | 86,702,869 |

| SSB | 8,733,239 | 9,315,835 | 582,596 | 132,934,165 |

| VIB | 148,646,677 | 169,859,284 | 21,212,607 | -21,200,807 |

Macro context

Macro factors have continued to reflect strain in Vietnam’s economy.

Currency movements

One US dollar was buying 26,502 Vietnamese dong from Vietcombank as of August 31.

This was up from 26,390 on August 1, representing an increase of 112 dong or about .42 percent.

The local currency is now worth 3.7 percent less than it was at the start of the year.

Of note, toward the end of the month, the State Bank also announced that it would sell US dollars on forward contracts to some banks.

Government bond yields

Vietnam’s 10-year government bond yield had reached 3.689 percent by September 1.

This was up 22.7 basis points from the start of August and 62.1 basis points since the start of the year.

Inflation

Vietnam’s consumer price index, despite strong GDP growth (7.52 percent in the first half of the year), has remained relatively flat.

In July, it came in at 3.19 percent, which is actually just below the year-to-July average of 3.26 percent.

Given the strong GDP growth, this could indicate inflation is being artificially constrained, i.e. via price controls, and that may mean an inflation shock somewhere down the track.

Preliminary inflation figures for August should be available from the National Statistics Office on September 6.

Fund commentary

Of note, on the HoSE, derivatives and short selling are not permitted. Investors can only earn returns through dividends or rising share prices. This creates a structural bullish bias in the market that should be kept in mind when assessing market commentary.

PYN Elite

The Finnish fund, in a statement on August 22, argued 2025 could be a “Big Year” for equities, similar to past surges in 1999, 2003, 2009, and 2012.

Its argument centred around stronger government spending, abundant liquidity, bank lending support, resolution of U.S. tariff risks, and a potential FTSE upgrade to emerging-market status in October.

Asia Frontier Capital (AFC)

AFC, in its August Vietnam Fund Update, said it expects Vietnam’s economy to accelerate, fuelled by expanding credit, record FDI, and a US$48 billion infrastructure push.

On this basis, the fund sees the VN-Index advancing toward 1,800 points in the coming months, supported by banks, new IPOs, and strong corporate earnings.

Points of note

These are a few ongoing concerns that may not amount to anything, but are still worth being aware of.

Vingroup

Vingroup’s fundamentals do not look good, with rising debt and a dependency on cash injections from the group’s founder.

In this context, the continued increase in the company and its subsidiaries’ stock prices should be viewed with caution.

Credit growth

The banking sector is seeing strong growth in line with moves to dismantle credit growth caps.

These are not gone yet, but the general mood is that the more credit, the better and it seems that if limits are reached, there is a good chance they can be raised fairly easily.

Margin trading

At the end of June, outstanding loans through margin lending had reached VND 300 trillion or about US$11.4 billion, a record high, according to reporting from VietnamNet.

This would suggest that credit is playing a significant role in the current market rally.

Outlook

The HoSE is in an interesting place headed into September.

Liquidity is trending upward, driven by growing interest in the market on the back of stocks reaching all-time highs.

It’s not, however, clear that these stock prices are justified.

Moreover, in many cases — particularly in the case of Vingroup and its subsidiaries — they are moving counter to perceived wisdom.

That said, with 21 of 30 stocks in the VN30 rising in August, there is an opportunity here even if it is risky, and with continued significant withdrawals of foreign capital, there is room for foreign investors to buy, too.

Any moves, however, should be made with caution – there is ample evidence to suggest the current rally is fragile and that the recent, rapid acceleration is likely only temporary.