Vietnam’s stock exchanges have been slow to develop.

As a result, there are only a few products available, with trading generally limited to the basic buying and selling of stocks and bonds.

Reforms are, however, being passed frequently, and Vietnam’s key stock exchanges are slowly moving to be more in line with international stock market standards.

Furthermore, the frontier market status of Vietnam’s key exchanges has not been a deterrent for many foreign investors.

There are, of course, notable risks with investing in any developing market, though these risks are generally countered with higher potential rewards.

That said, foreign investors looking to invest in Vietnam’s key financial markets may be able to mitigate some of the risks by understanding the framework within which they operate.

With this in mind, this article runs through the key features of Vietnam’s securities trading system.

Vietnam Stock Exchange

The Vietnam Stock Exchange (VNX) is the umbrella organisation under which the Ho Chi Minh Stock Exchange (HoSE) and Hanoi Stock Exchange (HNX) operate.

It was established by the Law on Securities 2019 and is overseen by the State Securities Commission (SSC), which is a branch of the Ministry of Finance.

The VSX is responsible for managing Vietnam’s two principal stock exchanges: the HNX and the HoSE.

Hanoi Stock Exchange

The HNX replaced the Hanoi Securities Trading Centre (HSTC) through Decision 01 in 2009.

Its core functions are to manage Vietnam’s bond market and Unlisted Public Companies Market (UPCoM).

The Vietnam bond market

The Vietnam bond market is a part of the HNX and handles both government and corporate bonds.

Bonds in Vietnam have become a popular means of raising capital; however, over the past year or so it has been revealed that corporate bonds in several instances have been misused.

This has created some challenges selling bonds and has led to broad bond market reforms. It has also seen the size of the corporate bond market contract.

The Vietnam Unlisted Public Companies Market

Vietnam’s UPCoM handles smaller firms that wish to sell shares and raise capital but that do not qualify for listing on the HoSE.

In this light, Vietnam’s UPCom has become a pivotal stepping stone for businesses looking to list on the HoSE.

It has also become a fallback for firms that fail to meet HoSE standards – Local English learning conglomerate APAX Holdings, for example, was delisted from the HoSE in 2023 for failing to meet HoSE information disclosure requirements and reverted back to the UPCoM.

Generally, a company can list on the UPCoM as long as it is a public company.

This distinction is based on the charter capital and the number of shareholders or whether or not it has undertaken an initial public offering through the State Securities Commission.

📈GUIDE: Getting started with trading on Vietnam’s stock exchanges

At the end of January 2026, the Ho Chi Minh Stock Exchange recorded 45,792 accounts held by foreign individuals and 6,359 by foreign institutions — a clear sign of growing global interest in Vietnam’s fast-evolving equity market.

While opening a trading account can unlock exciting opportunities in sectors ranging from tech to consumer goods, the process isn’t always straightforward.

Foreign investors must navigate documentation requirements, understand local custodial systems, and comply with ownership limits on listed stocks.

It’s important to prepare carefully, choose a reputable brokerage, and understand market practices before jumping in.

Getting these details right from the start helps avoid delays and ensures you’re ready to act when opportunities arise.

👉See: How to Open a Trading Account in Vietnam: Technical Guide

Ho Chi Minh City Stock Exchange

The Vietnam stock exchange that is most well-known and the most active is the Ho Chi Minh City Stock Exchange (HoSE).

This stock exchange has just over 400 listed companies, with the entire stock exchange having a market capitalisation of VND 8,534,134.89 billion (US$323,876,086,907) as of January 31, 2026.

The HoSE has been essential for many firms in Vietnam to raise capital to expand.

It is, however, relatively undeveloped and trades are mostly limited to buying and selling stocks.

Market manipulation and enforcement efforts

Vietnam’s main stock market has faced controversy in recent years with respect to market manipulation.

For example, allegations emerged in 2023 that the former head of the real estate firm FLC, Trinh Van Quyet, used family and friends to jack up the price of FLC stock, netting the high-profile executive US$176.2 million.

Of note, Trinh Van Quyet was sentenced to 21 years for fraud and stock market manipulation in August 2024.

Whereas this is the most high-profile case, it is apparent that this is a widespread practice in Vietnam.

The authorities in recent years have, however, made some effort in stamping it out.

Key stock market indexes in Vietnam

Like most stock markets, the Ho Chi Minh City Stock Exchange has a number of different indices across different sectors.

The two main stock market indexes in Vietnam, however, are the VN-Index and the VN30.

VN-Index

The VN-Index is a market capitalisation-weighted index of all of the stocks listed on the Ho Chi Minh Stock Exchange.

This is the main index used to measure the exchange.

It is the Vietnamese equivalent, for news reporting purposes, of the Dow Jones in the USA, Australia’s All Ordinaries, or London’s FTSE100.

VN30

Less talked about than the VN-Index, but by many measures just as important as the VN30.

The VN30 is a basket of 30 of the highest-performing stocks on the HoSE.

For investors who prefer diversified exposure, several ETFs track the VN30, offering access to Vietnam’s top-performing stocks without needing to invest in each company individually.

See also: Vietnam Stock Market Indexes: VN-Index, VN30, MSCI & FTSE

Vietnam stock market trading hours

Whereas more developed stock exchanges tend to trade from 10 am to 4 pm.

Vietnam’s major exchanges are slightly different. Trading on both exchanges is limited to about four hours and divided into two sessions.

HoSE

The HoSE is open Monday through Friday from 8:00 am to 11:30 am and from 1:00 pm to 5:00 pm.

Trading, however, is only conducted in the morning between 9:15 am and 11:30 am, and in the afternoon between 1:00 pm and 2:30 pm local time.

HNX

The HNX is open Monday through Friday from 8:00 am to 5:00 pm, with trading conducted from 9:00 am to 11:30 am and 1:00 pm to 2:30 pm local time.

Foreign investment in securities firms

Foreign investors may participate in Vietnam’s securities market by acquiring stakes in securities trading firms.

However, ownership limits depend on whether the investor is an individual or an organisation and whether certain qualifying conditions are met.

Foreign ownership limits in securities trading firms in Vietnam depend on whether the investor is an organisation or an individual.

An individual and their immediate family can own no more than a collective 49 percent of a securities firm, whereas an organisation can own 100 percent of a trading firm if it meets the following criteria:

- It has been operating in the field of banking, securities, and/or insurance for at least two years;

- The licensing authority in the organisation’s home country and the State Securities Commission in Vietnam have a mutual or multilateral agreement on information exchanges, management, inspection, and supervision of their respective securities markets and activity carried out on those markets;

- The organisation has recorded a profit for the last two years; and

- The organisation’s latest annual financial statement has been audited and has received an unqualified opinion.

Organisations that do not meet these criteria can still invest in securities trading firms, but, like individual investors, cannot own more than 49 percent.

This is outlined in Article 77 of the Law on Securities.

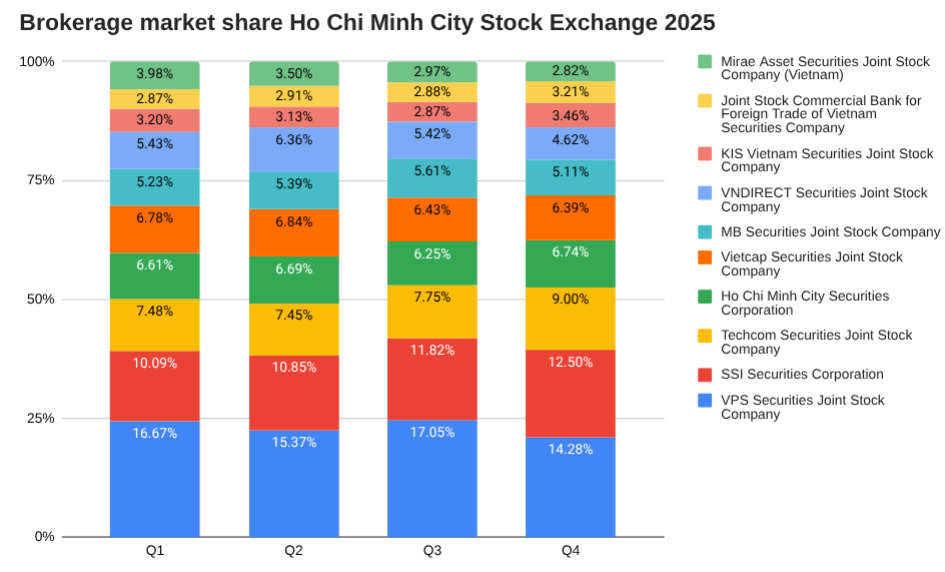

Vietnam securities firms by market share, 2025

| Company | Q1 | Q2 | Q3 | Q4 |

| VPS Securities Joint Stock Company | 16.67% | 15.37% | 17.05% | 14.28% |

| SSI Securities Corporation | 10.09% | 10.85% | 11.82% | 12.50% |

| Techcom Securities Joint Stock Company | 7.48% | 7.45% | 7.75% | 9.00% |

| Ho Chi Minh City Securities Corporation | 6.61% | 6.69% | 6.25% | 6.74% |

| Vietcap Securities Joint Stock Company | 6.78% | 6.84% | 6.43% | 6.39% |

| MB Securities Joint Stock Company | 5.23% | 5.39% | 5.61% | 5.11% |

| VNDIRECT Securities Joint Stock Company | 5.43% | 6.36% | 5.42% | 4.62% |

| KIS Vietnam Securities Joint Stock Company | 3.20% | 3.13% | 2.87% | 3.46% |

| Joint Stock Commercial Bank for Foreign Trade of Vietnam Securities Company | 2.87% | 2.91% | 2.88% | 3.21% |

| Mirae Asset Securities Joint Stock Company (Vietnam) | 3.98% | 3.50% | 2.97% | 2.82% |

Vietnam stock exchange trading restrictions

Trading on Vietnam’s stock exchanges is heavily regulated and comes with a number of limits and restrictions.

Without going into detail on all of the minor nuances, there are two key restrictions foreign traders and investors should be aware of.

These are foreign ownership limits and limits on how high or low a stock can go in a single day.

Foreign ownership limits in Vietnam securities

Vietnam’s foreign ownership limits are generally specific to particular industries and business lines.

For investing in Vietnam’s securities industry, they are outlined in Decree 155. According to the decree, the foreign ownership limit in a particular stock is determined in one of four ways.

- In the first instance by any international treaty to which Vietnam is a signatory. For example, the CPTPP allows for member states to own up to 65 percent of a facilities-based telecommunications service in another member state.

- If there is no international treaty, then foreign ownership is determined by any domestic law pertaining to a specific business line. For example, the Law on Insurance Businesses states that foreign investors can own up to 100 percent of the shares in an insurance firm.

- For restricted business lines, if no limit is specified, the cap is 50 percent; and

- If a business has multiple business lines, the cap is the lowest foreign ownership limit among the group.

Note that these limits are somewhat restrictive for local firms in attracting capital and for foreign investors in their ability to influence key decision makers in an organisation.

They have also been cited as one reason that Vietnam is still listed as a frontier market by FTSE Russell and MSCI.

This is discussed in more detail below.

These restrictions can limit the ability of foreign investors to take controlling stakes or exert influence over business decisions.

They also reduce liquidity in stocks that reach their foreign ownership limits, making them less attractive to international investors.

As of March 11, 2024, of 401 stocks listed on the HoSE, 371 stocks had foreign ownership limits. For 366 of those stocks, foreign ownership was capped at 50 percent or less.

Foreign room limits

While foreign ownership limits set the maximum percentage of a company that foreign investors are allowed to hold, foreign room limits refer to the remaining available space under those caps.

In other words, even if a stock is legally allowed to have 49 percent foreign ownership, the actual foreign room may be far lower—or even zero—depending on current holdings.

Once a company’s foreign room is full, no additional foreign buying can take place unless existing foreign shareholders sell, often creating bottlenecks for high-demand tickers.

Monitoring these limits is critical for institutional and retail investors alike, as foreign room availability directly affects trade execution and portfolio strategy.

You can view the latest real-time data on foreign room across all listed Vietnamese companies here.

For the latest foreign room limits, see: Vietnam Foreign Room Limits: Latest Update

Vietnam stock exchange trading bands

In Vietnam, there are limits on how high a stock can rise and how low it can fall in a single day

On the HoSE, it is 7 percent either side of the reference price, which is the closing price from the day before.

This is, however, extended on the first day of trade for new stocks to up to 20 percent either way–this also applies to stocks that have been suspended for more than 25 days.

On the HNX, it’s 10 percent either way and can be up to 30 percent for newly listed stocks or stocks that have been suspended for more than 25 days.

And on UPCoM, it’s 15 percent either way normally, and can be up to 40 percent on the first day of trade or on the first day back after a stock has been suspended for more than 25 days

Challenges and future prospects

While Vietnam’s stock market has made impressive strides in attracting investors and integrating globally, it still faces a range of structural and operational challenges.

At the same time, ongoing reforms, technological upgrades, and strong economic fundamentals present significant opportunities for future growth.

Market status

The HoSE is considered a frontier market by the world’s two major market index providers: the United Kingdom’s Financial Times Stock Exchange (FTSE) Russell and the United States’ Morgan Stanley Capital International (MSCI).

These two index providers each have their own reasons for Vietnam’s status as a ‘frontier market’ as opposed to an ‘emerging market’.

Note that the HoSE meets the quantitative metrics of both firms. It is the qualitative metrics (listed below) that are holding the local bourse back.

FTSE Russell

FTSE Russell announced in October of 2025 that Vietnam is set to be reclassified from a Frontier to a Secondary Emerging market effective 21 September 2026, pending an interim review in March 2026.

The decision follows reforms in 2024 that removed the pre-funding requirement for foreign institutional investors and introduced a formal process for handling failed trades, meaning Vietnam now meets all technical criteria under the FTSE Equity Country Classification Framework.

See also: Vietnam’s Stock Market Upgrade Opportunity: Unpacked

There are two main criteria preventing the HoSE from meeting FTSE Russell emerging market status. These are:

Foreign traders currently need to prove they have the funds to pay for a share purchase before a trade can be completed (this has changed since FTSE Russells last review. Any impact should be reported in its March 2024 update); and,Foreign ownership limits are too excessive.

The HoSE aims to meet FTSE Russel’s emerging market criteria in 2025.

Of note, it’s estimated that an upgrade of the market could generate in the vicinity of US$10 billion in additional investment for Vietnam’s main stock exchange.

MSCI

Whereas the FTSE Russel has only a few criteria left for Vietnam to fulfil, MSCI had at least nine criteria in June of 2025.

These were:

- foreign ownership limits;

- remaining room for foreign investment;

- equal rights for foreign investors;

- degree of freedom in the foreign exchange market;

- ease of registration and account opening;

- market regulations;

- information flows;

- clearing; and

- transferability.

It has been widely argued (though not at all confirmed) that Vietnam can meet FTSE Russell’s requirements by the end of 2025.

There does, however, appear to be a plan for tackling the remaining MSCI criteria and as such there is no apparent timeline.

Korean Stock Exchange (KRX) System

Vietnam’s Ho Chi Minh City Stock Exchange (HoSE) officially launched its new KRX trading system, ten years after it was first conceived, in May of 2025.

This has significant potential for the development of Vietnam’s securities trading ecosystem.

Key improvements include:

- Order matching reform: ATO/ATC orders no longer have priority over earlier limit orders and now display prices like regular orders

- Order editing: Price or volume increases reset time priority; volume decreases do not

- Market order changes: MP orders replaced by MTL (Market-To-Limit); unmatched volume converts to limit order at ±1 tick

- Odd lot trading expanded: Can now be traded continuously from 9:00 to 14:45

- Negotiated trading update: Both buyer and seller can initiate and confirm trades

- Foreign investor room: Now updates immediately upon order placement

The KRX system is a long-awaited leap forward for Vietnam’s stock market, boosting transparency, bringing it more in line with international practices, and positioning the stock market to attract deeper institutional investment flows.

International integration timeline

Vietnam’s stock market has taken major steps towards global integration in recent years, signalling its ambition to become a more open, credible, and competitive destination for international investors. These include:

- In April of 2021, Vietnam officially became a part of the Asian and Oceanian Stock Exchanges Federation.

- In September of 2023, the Vietnam Stock Exchange officially ascended to the World Federation of Exchanges.

Vietnam’s stock exchange compared to region

Vietnam’s stock market is one of the fastest-growing in Southeast Asia but remains classified as a frontier market.

It has expanded rapidly in both market capitalisation and trading activity, driven by retail investors and state-linked enterprises.

Here’s how it compares to other stock exchanges in the region.

Indonesia

Indonesia’s exchange is larger and more liquid than Vietnam’s, with deeper institutional participation.

Vietnam’s market is catching up in trading volume but still lacks Indonesia’s depth and foreign investor diversity.

Learn more about Indonesia’s stock exchange→

Thailand

Thailand’s exchange is more mature and stable, supported by long-established regulatory systems and professional investors.

Vietnam’s bourses are newer and more volatile but offer higher growth potential.

Discover more about the Stock Exchange of Thailand→

Malaysia

Malaysia’s stock market is bigger and more developed, with stronger governance and international integration.

Vietnam trails in institutional investment and market transparency but leads in growth momentum.

Explore Malaysia’s stock exchange→

Singapore

Singapore’s exchange serves as the regional financial hub with high foreign listings and global capital flows.

Vietnam’s market is more domestically focused and is still building credibility among international investors.

Philippines

The Philippines’ market is comparable in size but less dynamic than Vietnam’s in terms of new listings.

Vietnam attracts stronger retail participation, while the Philippines maintains steadier, more conservative trading patterns.

Find more information on the Philippines stock market→

What’s next?

Vietnam’s stock exchanges are still in a state of flux but they are headed toward becoming more developed and accessible for foreign traders.

Effective and profitable trading, however, can best be achieved with the right up-to-date and relevant information.

In this respect, investors looking to trade on the Ho Chi Minh Stock Exchange should make sure to subscribe to the-shiv.

First published December 3, 2023. Last updated February 9, 2026.