In November, Vietnam’s key indexes continued to climb, though largely on the back of a standout performance from Vietnam’s biggest conglomerate by market capitalisation, Vingroup (VIC), which gained 36 percent.

This was despite Vingroup’s Q3 consolidated financial statements revealing its already precarious financial situation had deteriorated further, with its debt at 5.7 times equity in Q3, up from 5.1 in Q2, and its subsidiary VinFast reporting a third-quarter net loss of VND 24 trillion or US$910 million.

With this in mind, whereas the market showed a solid performance at a glance, its November results should be viewed with an air of caution.

The VN-Index

The VN-Index climbed 51 points or 3.13 percent in November.

This was a change for the index, which recorded slight declines in both September and October.

Market Capitalisation

The market capitalisation of the Ho Chi Minh City Stock Exchange as of Friday, November 28, was just under VND 7.5 quadrillion or US$284.6 billion.

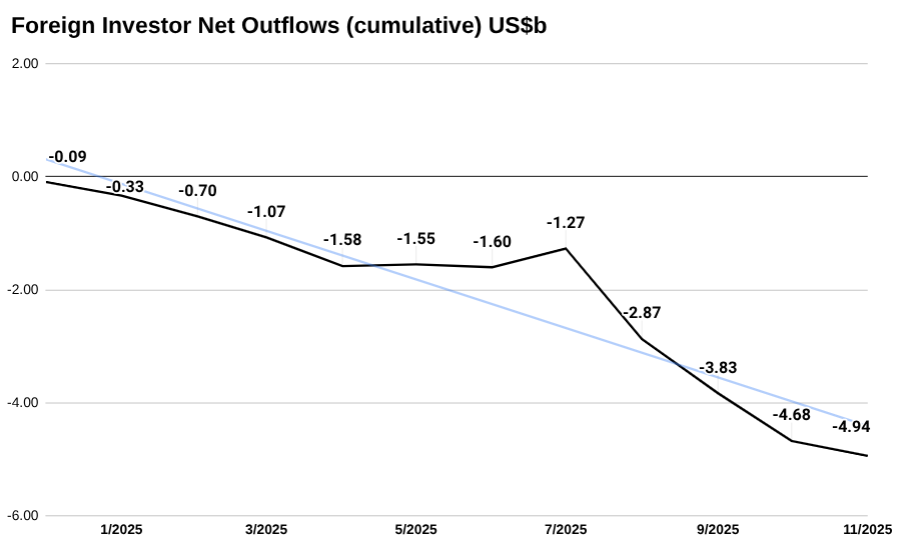

Foreign investor flows

In total, foreign traders net sold US$262.3 million in November.

Shares most sold by foreign traders, in volume terms, included: Military Bank (MBB), Sacombank (STB), Asia Commercial Joint Stock Bank (ACB), Vincom Retail (VRE), and SSI Securities (SSI).

Shares most bought by foreign traders include: HDBank (HDB), Hoa Phat Group (HPG), TPBank (TPG), Vinamilk (VNM), and FPT Corporation (FPT).

Trading activity

Liquidity fell sharply in November, averaging just VND 20.09 trillion or US$762.1 million compared to VND 31.1 trillion or US$1.18 billion in October.

This was a significant fall compared to the preceding four months, though it brings the market back in line with historical norms.

Macro context

Government bond yields

Vietnam’s 10-year government bond yield inched higher, closing out November at 4.049 percent, up from 3.954 percent at the end of September.

This represents an increase of 9.5 basis points, with the total increase over the last twelve months now sitting at 118.8 as of December 1.

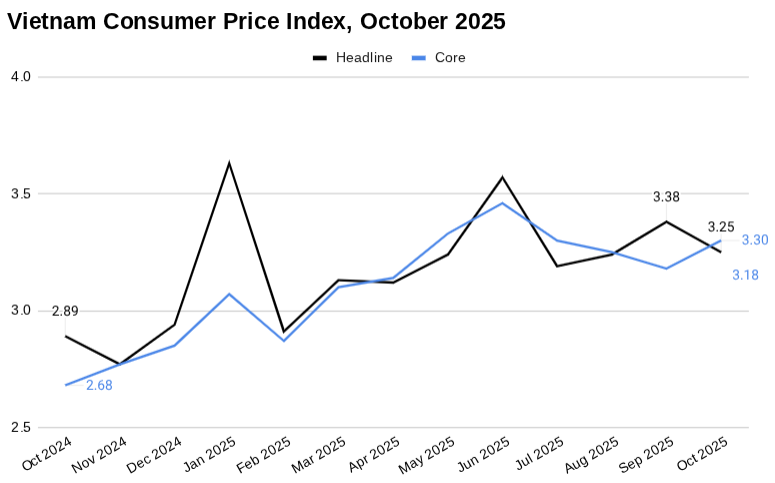

Inflation

Vietnam’s consumer price index (CPI) rose by 0.20 percent in October 2025 compared with September, driven mainly by higher food prices in flood-affected areas and increased tuition fees at private schools, according to the latest data from the National Statistics Office (NSO).

The CPI rose 2.82 percent from December 2024 and 3.25 percent year-on-year.

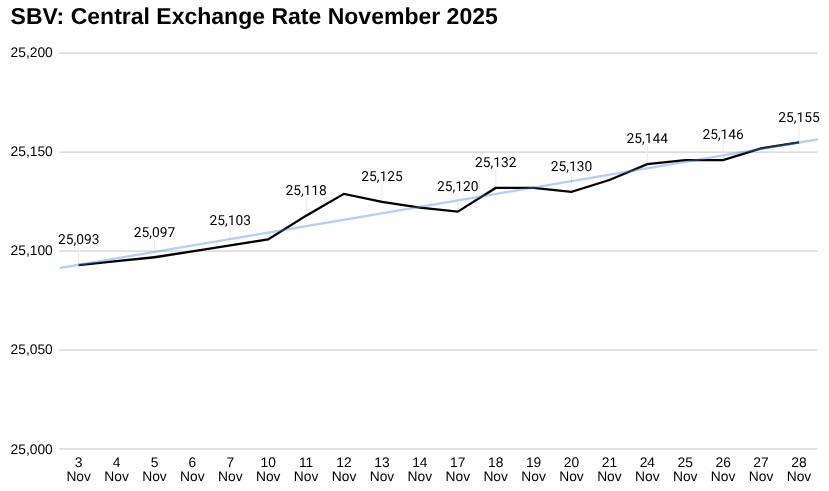

Currency movements

The State Bank of Vietnam allowed the local currency to weaken against the greenback to the tune of 62 dong in November.

Conversely, the black market rate strengthened a little, with the mid-market rate falling from VND 27,775 to the US dollar to 27,690 by the end of the month.

In spread terms, the difference between the unofficial mid-market rate and the State Bank’s central exchange rate was 10.89 percent at the end of October. This gap closed a little in November, sitting at 10.08 percent by the end of the month.

Of note, the State Treasury made at least two purchases of US dollars. One on November 11 worth US$100 million and another on November 27 worth US$150 million. It was not clear what these purchases were for.

December outlook

With Christmas just weeks away, exports are slowing down; however, coming up on the Lunar New Year in February, consumer spending should increase and, by extension, consumer goods stocks.

On that note, with the banking sector’s loan-to-deposit ratio currently sitting at around 110 percent, a risky position to be in by any assessment, it will be interesting to see what happens as consumers dig into their savings to cover their holiday expenses.

As for Vingroup, its stock is now up over 400 percent since January.

This has pulled up Vietnam’s key indexes, which, whether driven by just one stock or many, can have a significant impact on investor psyche, with hype often cited as a key driver of market growth.

This largely links the future performance of the local bourse to Vingroup shares and they look set to continue to move to a beat of their own.

(US$1 = VND 26,350)