Manufacturing in Vietnam is feeling the heat from higher input costs on rising fuel prices. This has led the sector onto rocky ground, with new orders falling and increased costs eating into profit margins.

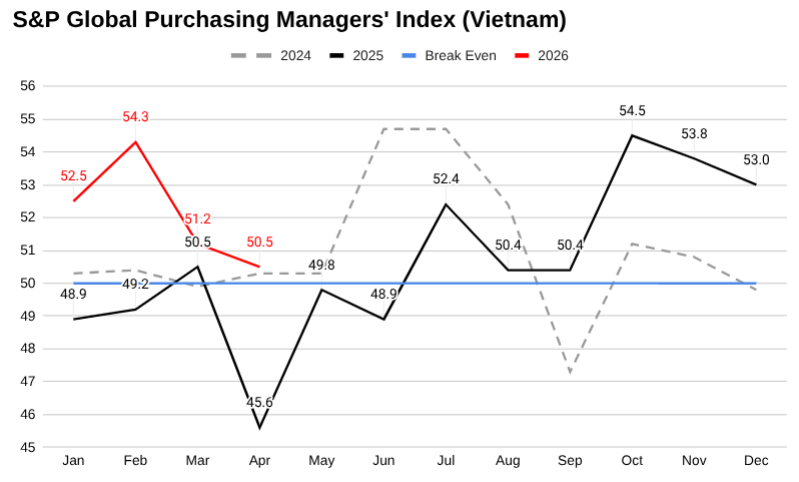

S&P Global’s Purchasing Managers’ Index fell from 51.2 in March to 50.5 in April. This still reflects growth in the manufacturing sector, though it is the lowest the index has been since September 2025, and is part of a downward trend on the back of price and supply disruptions caused by the conflict in the Middle East.

What this looked like in practice, S&P found, was a decrease in new orders, with manufacturers surveyed reporting cost-cutting measures including lowering their headcounts, reducing staff hours, and cutting back on inventory.

The downturn, however, has not necessarily been uniform across industries, with Chris Walker from Vietnam Factory Tours telling the-shiv that the garment and textile industry is still going strong.

“I would say Vietnam is still the first choice for anybody that wants to do apparel manufacturing… and therefore we’re still getting a lot of inquiries,” he said.

Vietnam’s garment and textile exports fell 2.35 percent in April over March in terms of value, though they were up about half a percent against April of last year.

Cotton imports, meanwhile, were up 21 percent in both volume and value in April, potentially signalling expectations of future orders.

Walker did note, however, that traditionally cheaper polyester fabrics are made using petrochemical inputs and are therefore becoming more expensive, making natural fibres more competitive.

In this context, the increase in cotton imports could also simply be indicative of a shift in material preferences.

That aside, whereas demand might be steady, input costs are edging higher. Passing on these costs, however, is difficult, Walker says.

“The Targets, the Walmarts, all the retailers, they have to make the consumer happy… And the consumers don’t want to pay a premium for the war.”

“So then it means that the retailers or the buyers have to give up some of their profit margin, and then they insist that the rest of the supply chain give up their profit margin.”

Similarly, an industrial manufacturing expert, who wanted to remain unnamed, told the-shiv that only marginal price increases have been noted thus far, with businesses forgoing some profit to prioritise keeping the doors open instead.

“By and large, I’m seeing manufacturers quote at prices that they think they can manage, just to keep orders on,” they said.

But whereas they had some concern about rising fuel prices, they were more worried about long-standing challenges facing the sector, including the limited value added locally, a lack of domestic demand, rising interest rates, and unsettled electricity policy raising power shortage risks.

They pointed to these factors driving mergers and acquisitions, but also some firms entirely out of business.

That is to say, this latest disruption may accelerate longer-term consolidation trends already visible in Vietnam’s manufacturing sector — analysis of Vietnam customs data by the-shiv back in October of 2025 found a significant shift in the mix of domestic and foreign invested enterprise (FIE) exports from a split of roughly 30/70 in favour of FIEs in October of 2024 to roughly 20/80 a year later.

That aside, there are some signs that the current fuel price challenges could create a short-term boost to the sector.

In an article published on its website last week, shipping and logistics firm Metro Shipping noted that the prospect of fuel prices continuing to rise is seeing firms begin to shift toward frontloading deliveries.

“A growing number of importers are moving cargo earlier amid concerns that operational disruption, congestion and capacity shortages could intensify later in the year,” it said.

Notably, a similar approach to the Trump administration’s “reciprocal” tariff regime was widely reported last year. This past experience could further inspire firms to head in this direction, now familiar with how the necessary supply chain adjustments might be made.

Still, if elevated fuel prices persist, the risks to Vietnam’s manufacturing sector will become increasingly difficult to ignore.

This could have wide-reaching implications, too, with about a quarter of Vietnam’s GDP derived from the sector last year.

It’s also one of Vietnam’s biggest employers and a strong draw card for foreign direct investment, which has been instrumental to Vietnam’s economic growth in recent years.

How the manufacturing sector responds to and weathers the fuel crisis, therefore, will be a telling indicator of how the economy might fare on the whole.