Contents

ToggleDisclaimer: The author of this Outlook does not own any stocks or have any financial interest in the performance of any of Vietnam’s stock markets.

In October, it was announced that FTSE Russell would upgrade the Ho Chi Minh City Stock Exchange from a frontier to a secondary emerging market in September 2026 if all went well in its next review.

This, however, didn’t seem to change investor sentiment all that much, with foreign investors continuing to exit the market and the VN-Index continuing to slip.

An announcement in which the Government Inspectorate named a number of firms for bond-issuance violations didn’t help either.

It’s in this framework that this Outlook reviews what happened in October and considers what this might mean moving forward into November.

It's free to keep reading but you will need to sign in.

The VN-Index

The VN-Index slipped a little in October, losing about 22 points.

This was in line with September, which also saw the key index shed about 19 points.

It was, however, in stark contrast to August, when the index recorded a 176.69 point gain.

This is noteworthy in that August’s huge gain was mainly attributed to Vingroup and its subsidiaries.

Their rapid growth, however, now appears to have tapered off with Vingroup gaining just 9.21 percent in September versus 21.61 percent in August, Vincom Retail gaining just 3.74 percent versus 8.19 percent, and VinHomes going backwards, shedding 3.69 percent, versus a gain of 16.11 percent.

These past growth numbers and significant weightings for these stocks in Vietnam’s key indexes have largely hidden a much more subdued stock market this year, which now appears to be coming through.

That is to say, the picture in September seems much more in line with expectations and with Vietnam’s regional counterparts.

Market Capitalisation

The market capitalisation of the Ho Chi Minh City Stock Exchange as of Friday, October 31, was just over VND 7.25 quadrillion or US$275.3 billion.

Of that, about 16 percent is attributable to foreign traders.

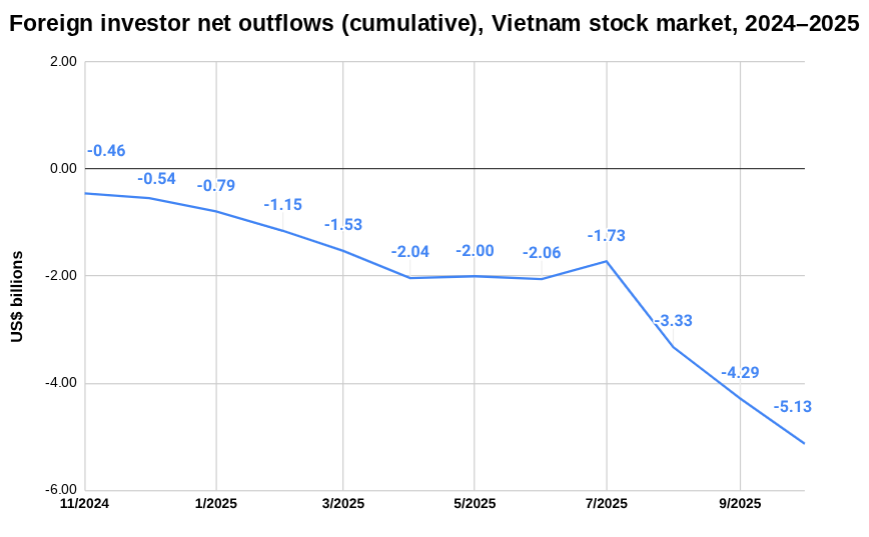

Foreign investor flows

Foreign traders continued to exit the local bourse in October.

In total, they net sold US$846.4 million.

This was despite the aforementioned FTSE upgrade, with media commentators at pains to point out that inflows from the upgrade are likely to be realised over time, not straight away.

Moreover, the timeline comes with caveats, in particular that a March review has to find everything up to par.

Shares most sold by foreign traders, in volume terms, in October included: Military Bank (MBB), SSI Securities (SSI), and Saigon – Hanoi Commercial Joint Stock Bank (SHB).

Shares most bought by foreign traders in October include: Vingroup JSC (VIC), LienViet Post Bank (LPB), and FPT Corporation (FPT).

Trading activity

Liquidity in October was almost identical to September, coming in at VND 31.1 trillion or US$1.18 billion a day, compared to VND 31.3 trillion or US$1.19 billion in September.

This is still significantly higher than normal.

From October last year to June this year, the average monthly trading volume was only VND 15.66 trillion or US$594 million.

Macro context

Government bond yields

Vietnam’s 10-year government bond yield inched higher, closing out October at 3.954 percent from 3.761 percent at the start of the month.

This represents an increase of 19.3 basis points over September, with the total increase over the last twelve months now sitting at 118.8 as of November 3.

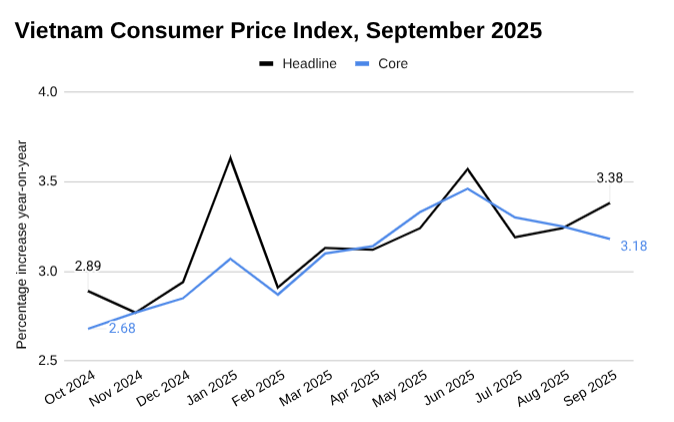

Inflation

Vietnam’s consumer price index (CPI) rose 0.42 percent in September 2025 compared to August, led by higher tuition fees, food prices, and housing maintenance costs, according to the National Statistics Office.

The CPI was 2.61 percent higher than in December 2024 and up 3.38 percent year-on-year.

Currency movements

The State Bank of Vietnam allowed the local currency to strengthen against the greenback to the tune of 94 dong in October.

Conversely, the black market rate weakened significantly, with the mid-market rate climbing from VND 26,615 to the US dollar to 27,825 by the end of the month.

In spread terms, the difference between the unofficial mid-market rate and the central bank’s peg was just 5.49 percent at the end of September, but blew out to 10.89 percent by the end of October.

In response, the SBV has enlisted the help of various ministries to crack down on the unofficial foreign currency trade.

It also sold another US$1.5 billion in 180-day cancellable forward contracts on 22 October — its third such move in less than two months.

This further chips away at an already risky, less than two months’ worth of imports in foreign currency reserves.

November outlook

Vingroup shares seem to be levelling off; however, their behaviour this year so far has been hard to explain. That is to say, there are no factors that would indicate they should go higher, but that doesn’t necessarily mean that they won’t.

Similarly, their Q3 financial statements show a company heavily saddled with debt, which might spook investors, though this has been apparent for a long time, and it hasn’t stopped its shares from climbing yet.

On the currency, a representative of VinaCapital said at a conference last week that they expect a rate hike to be on the cards in the near future.

This would make sense given the dwindling state of Vietnam’s Forex reserves, although they have been uncomfortably low for some time, but this hasn’t seen a rate hike yet.

That is to say, the market and economy don’t necessarily always follow received wisdom, and this can make it tricky to forecast what might happen next.

What is clear, however, is that there are factors that cannot continue as they have been, and as such, change is very likely on the horizon.

(US$1 = VND 26,350)