Unlike larger regional competitors with stronger balance sheets and greater pricing flexibility, Vietnam’s airlines are entering the latest fuel shock carrying heavy debt loads, operating under domestic airfare caps, and facing tighter funding conditions.

For Vietnam’s airlines, the conflict in the Middle East, and the volatility it has brought to supplies of jet fuel, is going to be a much bigger problem than it might otherwise be for other airlines elsewhere.

For one, it imports a lot of its jet fuel.

Most of this comes from China, and though Vietnam was given an exemption to reported export restrictions announced in March, there is still a heightened risk that if the shortage wears on too long, Chinese producers might need to prioritise domestic needs over foreign buyers.

Of course, there are other places to buy jet fuel; however, Vietnam’s airlines are also competing with much better capitalised airlines from developed economies like Australia, Japan, South Korea, and Singapore.

These carriers can pass on these costs to consumers relatively easily, too.

For Vietnam’s airlines, however, domestic ticket prices are regulated, with caps designed to ensure air transport remains accessible to as many people as possible.

A noble goal, the reality is that this prevents local airlines from maximising revenue when times are good, to cover shortfalls when times are bad, the current fuel crisis, for example

Moreover, Vietnam’s airlines are already heavily leveraged.

Vietnam Airlines, the national flag carrier, has survived post-COVID on government loans and debt forgiveness, only returning to positive equity last year after a major share issuance largely backed by the state.

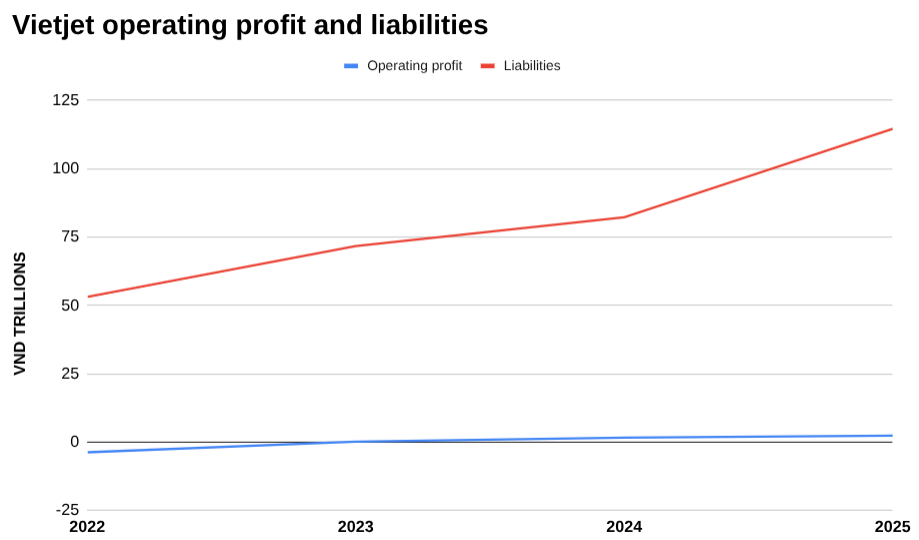

Budget carrier Vietjet has had its own financial woes too, with a court in the UK ordering the airline to pay US$181.5 million last year over a COVID-era leasing dispute. This has contributed to, at the end of 2025, the airline carrying liabilities equal to nearly 48 years of operating profit.

As for Bamboo Airways, as of July 31, 2025, it had outstanding short-term debts — a combination of fuel charges, bank loans, and ground services costs — of VND 9 trillion (US$341.6 million).

Vietravel Airlines has also had its own financial challenges after launching its first flight in January of 2021, in the middle of the pandemic. Its financial records are not public; however, local media reported losses in 2021, 2022, and 2023.

That is to say, funding higher jet fuel costs could present a significant financial burden, with funding options limited.

Notably, a share issuance has been floated for Vietnam Airlines, though Petri Deryng, Founder of Vietnam-focused PYN Fund Management, which holds a significant stake in the carrier, told the-shiv in an email that he believes an equity raising is unlikely.

“Q2 will be badly damaged due to the jet fuel price hike, but I don’t think the company will do any equity raising based on this situation, and instead they will cover this period from their own cash reserves and other government-related sources and other methods of short-term financing,” he said.

Vietjet shares are also up 88 percent over the last year, trading at about 4 times their book value. An unusually high multiple for an airline, it’s difficult to see where significant new buying demand comes from, if it were to look at raising additional capital through the stock market.

Accessing funds through the banking system could also be difficult with domestic banks already near the limits of what they can lend without breaching capital adequacy regulations. Interest rates are also already quite high, with rising inflation on the back of the increasing fuel prices, a strong impetus for interest rates to go higher.

Another idea that has been floated is raising foreign ownership caps.

Currently sitting at 34 percent it’s been repeatedly argued that this is not enough to give foreign investors the kind of input they need in an airline’s operations.

Vietjet and Vietnam Airlines, however, have both come out against the plan (this is despite Vietjet arguing for the change back in 2017).

It’s not clear what the aversion to a higher cap is; however, a foreign investor that could provide access to cheaper foreign capital could pose a significant threat to the status quo — as long as everyone is struggling, no one can pull ahead.

The bigger risk, however, is that domestic operational challenges weigh on these airlines’ international operations — losing international business customers or air cargo routes could have significant long-term impacts.

All of that is to say that Vietnam’s aviation industry is in a tricky spot when it comes to the currently high fuel prices, and coming out the other side unscathed will be challenging. Moreover, recovering quickly, if at all, will be difficult without significant industry structural reform.

The data

Vietjet operating profit versus liabilities, VND millions

| 2022 | 2023 | 2024 | 2025 | |

| Operating profit | -3,700,917 | 184,272 | 1,671,290 | 2,388,947 |

| Liabilities | 53,138,670 | 71,672,281 | 82,196,542 | 114,581,828 |