The oversupply of cars in Vietnam’s car market has been well known for some time, yet the gap between supply and demand continues to grow. Without a clear rationale for the lack of a market correction, it would make sense if car makers with other options were reconsidering their positions.

The arrival of the Mercedes-Benz factory in Ho Chi Minh City heralded the beginning of a revolution for Vietnam’s auto sector when it first started operating in 1997.

At the time, Vietnam’s GDP per capita was only US$449, barely a tenth of the US$4,470 it is today, according to IMF data. This meant that even the cheapest model was well out of the reach of most Vietnamese at the time.

This was, however, set to change as the economy slowly liberalised, culminating in admission to the World Trade Organisation in 2007.

The years that followed were a relatively good time for the Mercedes factory. They weren’t the best-selling cars, but they did okay, and as cars became more and more affordable, sales grew.

Fast forward to 2024, however, and with its lease on that factory running out, but the local authorities dragging their feet on an extension, the company announced that it was considering winding down its operations in Vietnam altogether.

Fortunately, at the 11th hour, higher powers stepped in, and the Mercedes-Benz lease was extended to 2030; the damage, however, may have already been done.

Indeed, the company, amid the uncertainty, had registered an import business in what looked like a way to keep a foothold in the market in the event its lease was not renewed.

This is noteworthy in that Vietnam has changed markedly since that factory first opened in 1997, with a series of free trade agreements removing import tariffs on cars entering the country, making local production less of a necessity.

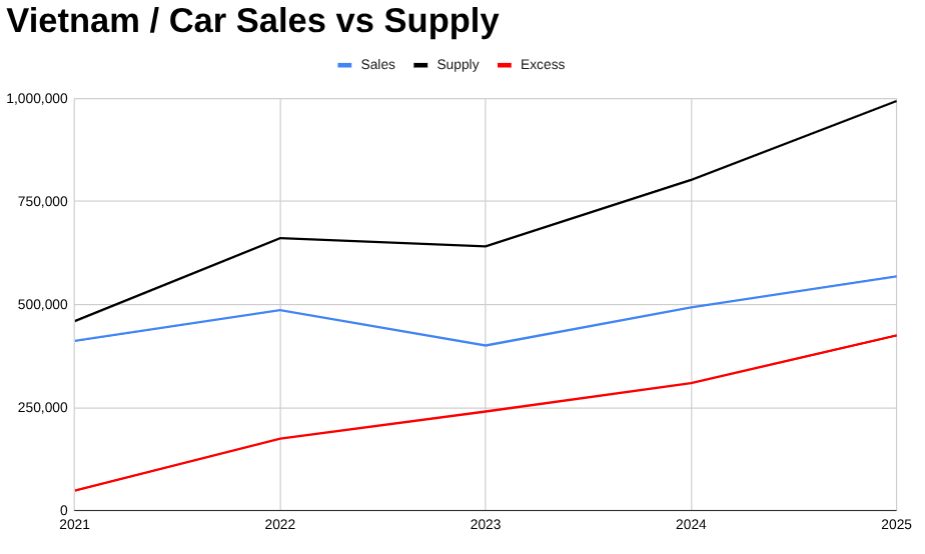

Moreover, the case for a local factory becomes even weaker when considering the size of the supply in the market versus new car sales.

Specifically, in 2025, on average, between imports, locally built vehicles, and leftovers from the year before, roughly 994,000 cars were available for purchase. However, sales and exports reached just 569,000 units, leaving a surplus of about 425,000 vehicles.

This was considerably higher than the surplus in 2021, which was just under 48,200.

Moreover, the rate at which the supply is increasing is far outstripping the increase in sales.

In 2021, there were around 1.12 cars available for every car sold. By last year, that figure had jumped to about 1.75, underscoring just how much the market imbalance has widened.

For consumers, this has been a good thing, putting downward pressure on prices.

It has also seen producers lobbying the government for incentives for car buyers to drive up demand, extensions of registration fee cuts for locally assembled and electric vehicles, for example.

Price cuts and incentives, however, can only drive prices so low and likely still not low enough to be affordable for most Vietnamese, with the average wage roughly VND 8.7 million (US$331) a month, and even the cheapest, smallest cars still running at about VND 200 million (US$7,800) new.

Add to that infrastructure capacity limits — narrow streets and a lack of parking space in the big cities, for example — or the very ready availability of cheap, ride-hailing services, and buying a car makes less and less sense.

The point being that this is a significant barrier to demand growth reaching a pace equal to that of the current supply, let alone exceeding it to mop up all those excess cars.

Reducing the new supply coming into the market, however, comes with significant drawbacks.

Clamping down on imports through tariffs, for example, would likely breach free trade agreements to which Vietnam is a party, risking retaliatory tariffs.

Reducing local production, as a matter of policy, is also likely to be politically unpalatable, with the sector employing thousands of people.

The point being that neither demand-side fixes nor policy tools are likely to resolve the imbalance quickly or easily.

All of that said, the market should really be taking care of this itself — distributors should not be importing cars they don’t think they can sell, and car makers should not be producing vehicles that they don’t think the market can absorb.

In this context, the uncertainty surrounding Mercedes-Benz’s factory lease may be less of an isolated administrative problem and more of a stress test of whether local assembly is still economically justified.

Put another way, the supply–demand dynamics in Vietnam’s car market do not make a lot of sense, and under these conditions, it is reasonable to expect large international brands to reassess their long-term positions in the market.

The data

Table: Vietnam car supply 2021 – 2025

| 2021 | 2022 | 2023 | 2024 | 2025 | |

| Produced | 299,800 | 439,600 | 347,400 | 388,500 | 484,500 |

| Imported | 160,035 | 173,467 | 118,942 | 173,423 | 200,218 |

| Carried over | – | 48,172 | 174,705 | 240,439 | 309,374 |

| Total | 459,835 | 661,239 | 641,047 | 802,362 | 994,092 |

Table: Vietnam car sales 2021 – 2025

| 2021 | 2022 | 2023 | 2024 | 2025 | |

| VAMA | 277,203 | 358,063 | 276,377 | 295,979 | 313,359 |

| VinFast | 35,723 | 22,924 | 34,855 | 97,399 | 175,099 |

| Hyundai | 70,518 | 81,582 | 67,450 | 67,168 | 53,229 |

| Mercedes | 5,887 | 7,925 | 6,906 | 6,906 | 7,246 |

| Exports (tons) | 22,332 | 16,040 | 15,226 | 25,604 | 19,801 |

| Total | 411,663 | 486,534 | 400,814 | 493,056 | 568,734 |

Notes on the data:

- VAMA = Vietnam Automobile Manufacturers Association.

- Vinfast, Hyundai, and Mercedes-Benz Data from media reports / company websites (links embedded).

- There are other car companies that don’t report — actual total sales may be slightly higher than stated.

- Mercedes-Benz data 2023, 2024, and 2025 are estimates using averages of the preceding three years.

- Export data is from Trade Map with 2025 data an average of 2021 – 2024.

- Raw export data is in tons. Conversion used: 1 ton = 1 car.

- Imports are preliminary data from Vietnam’s General Department of Customs.

- Production data from National Statistics Office.